New Tax Year Has Started!

A new tax year will start 6th April 2026 and runs until the 5th April 2027 next year! Therefore, this is exactly the question we are encouraging all of our clients to ask themselves at this time of year: How much should I pay myself in the 2026 to 2027 Tax Year?

Indeed, we run a Tax Planning consultation process with each of our clients at this time every year. And as part of this process we provide them with a tax calculator which incorporates the updated tax rates and allowances which were announced by the Chancellor in the Autumn Budget. This allows our clients to experiment with and see the impact of paying themselves different levels of salaries and dividends from their limited companies. It also works for Employees and Self-Employed Sole Traders by incorporating employment and self-employment income. In addition to this useful tool, our clients have the opportunity to speak with one of our Accountants to discuss their specific circumstances. And for those that require additional pension, life insurance, or wealth advice, we have a partnership agreement in place with Boolers to provide specialist advice in these areas.

This allows us to help each of our clients based on their personal circumstances, and gives them the opportunity to instruct us what salary they would like us to process on their behalf for the new tax year on a more informed and knowledgeable basis.

Autumn Budget – Significant Changes

Significant changes proposed by the Chancellor in the Autumn 2025 Budget, which impact the decision for the coming tax year include:

- From 6 April 2026, the tax payable on dividends is set to increase by 2% for Basic and Higher rate taxpayers, to 10.75% and 35.75% respectively. The Additional Rate of 39.35% remains unchanged.

- Personal tax thresholds – i.e. Personal allowance, basic and higher-rate thresholds for income tax remain frozen until April 2031.

Other Key Information

Other key information which impacts the decision for typical taxpayers:

- Taxpayers (with the exception of those who earn more than £100k) start paying income tax when their salary exceeds the value of the Personal Allowance (£12,570). Where you earn more than £100k your personal allowance is reduced by £1 for every £2 of income in excess of this limit, so you start paying tax sooner.

- Employees start paying Employee’s National Insurance when their salary exceeds the Primary Threshold (£242 Weekly, or £12,570 Annually).

- Employers start paying Employer’s National Insurance when an employee’s salary exceeds the Secondary Threshold (£96 Weekly, or £5,000 Annually), unless they qualify for the Employment Allowance, in which case this will reduce the value of tax payable.

- Taxpayers start accruing National Insurance benefits (such as qualifying payments towards the State Pension) when their salary exceeds the Lower Earnings Limit (£125 Weekly, or £6,500 Annually).

- Eligible employers can use the Employer’s Allowance (£10,500) to offset the value of Employer’s National Insurance which is payable. There are strict eligibility criteria that apply in order to claim this, but typically you must have more than one employee earning above the Secondary Threshold ((£96 Weekly, or £5,000 Annually). So, businesses which have only a single Director (employee) are specifically excluded.

- Taxpayers start paying tax on dividends when their value exceeds the Dividend Allowance (£500).

- Businesses are taxed at:

- Small Profits Rate of 19% – On profits up to £50k

- A variable Marginal Profits Rate (between 19% and 25%) – On profits between £50k and £250k. Note – The “marginal rate” of tax (i.e. the tax you can save by reducing profit by £1 within this range) is 26.5%!

- Main Rate of 25% – On profits above £250k

- Note – Where there are associated companies these limits are reduced proportionally, resulting in higher rates of tax being applied at much lower levels of profitability.

Sole Traders

Due to the increase in Employer’s NI for salaries in the 2024 Budget, and a similar increase to dividend taxes in the current 2025 Budget, it is now paradoxically more tax efficient for certain taxpayers to operate on a self-employed basis as a sole trader. This is because the Government haven’t (yet) increased Class 4 NI by a similar value.

Operating as a sole trader does have significant limitations though when compared to running your own limited company. For instance, Sole Traders do not have the flexibility to:

- Choose how much you are paid.

- Choose the structure and method by which you are paid.

- Allocate dividends to a partner or other shareholders.

- Grow wealth tax efficiently within your limited company.

- Qualify for additional business expenses.

- And critically there is no limited liability.

As such we would not typically recommend this as an option to clients, unless they specifically request it.

Nevertheless, for certain taxpayers who operate independently and extract EVERYTHING that they earn each tax year (a good example is taxpayers who currently use an umbrella company and withdraw all of their earnings as a salary). Then operating as a sole trader may be the best option. It is also a good option for “additional” income streams, whereby you can operate your main business via your limited company so that you retain all the benefits of being incorporated, and also run a side hustle on a self-employment basis.

Limited Companies

For limited company clients the tax changes in recent years do now make the salary / dividend decision (and also the whole tax system) much more complex!

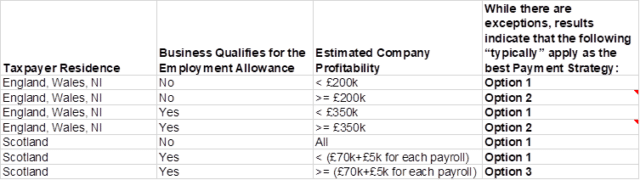

In summary, the most tax efficient salary now depends on:

- Your Country of Residence – Scottish taxpayers pay income taxes at different rates from the rest of the UK.

- Whether You Employ Other Staff and Qualify for the Employment Allowance – Qualifying for the Employment Allowance means that you can save up to £10.5k in Employer’s NI each tax year.

- The Profitability of Your Company – Companies now pay different rates of Corporation Tax depending on the profitability of their business.

Payment Strategies

Taking these factors into account we have examined a number of different Payment Strategies (assuming that all profits are extracted for comparison purposes), including:

- Option 1 – A salary and dividend strategy, setting salary at the value of the personal allowance of £12,570, and taking the rest as dividends.

- Option 2 – A salary and dividend strategy, setting salary at a value that reduces total company profitability down to £50k (so the company is only taxed at 19%), and taking the balance of £50k as dividends. Note – This method is NOT viable where there are associated companies, because higher rates of tax are applied at much lower levels of profitability.

- Option 3 – A salary and dividend strategy where you employ other staff and the company qualifies for the Employment Allowance. This strategy sets salaries at a level that fully utilises the Employment Allowance (i.e. £70k in total plus an additional £5k for each salary run), and taking the balance as dividends.

- Option 4 – A full salary strategy.

One of the obvious challenges of applying Option 2 is that you wont know for sure what the profitability of your company will be until the financial year is over and the company accounts have been produced. Additionally, it may not be practical to wait until this point to pay yourself a salary. So, if you want to apply this strategy you will need to estimate the profitability of your company for the next financial year that starts on or after 6th April 2026, and potentially adjust your salary or pension after the financial year end to accommodate the final position.

Results

We have compared the total tax payable for each of these strategies at £50k increments of company profitability. And while there are some exceptions to these rules, our results indicate that the following “typically” apply:

Note – Where it is not viable to apply Option 2 because there are other associated companies, continue to apply Option 1.

Please also note that:

- This comparison assumes that ALL profit is withdrawn. In practice this will rarely (if ever) be the case, and any funds retained within a limited company will represent significant value in terms of deferred tax, and also wealth creation!

- Pensions are another good way of reducing company profits (instead of paying yourself a salary) down to the £50k level which have no immediate tax impacts!

Please remember though that each client’s circumstances are different and there may be exceptions to what has been outlined above based on your specific circumstances, and also your preferences with respect to the salaries you specifically want to pay your staff.

Please also be aware of your legal responsibilities as an Employer (https://www.gov.uk/contract-types-and-employer-responsibilities ). In particular, please ensure that you set salaries that are compliant from a National Minimum Wage, National Living Wage, and Workplace Pension perspective if you employ other staff!

Can QAccounting Help Me?

Yes, we aim to be the UK’s Premier Online Accountancy and Tax Accountant, and we are here to help you every step of the way, whether you need to understand the rules in greater detail or need advice about next best steps.

Please give us a call (0116 243 7868), email us, or contact us ONLINE to speak to a member of our Accounting team without delay!

Author: George Ian Hope BAcc(Hons), MSc(IT), FCCA, CGA, CPA

Managing Director – QAccounting Limited (www.qaccounting.com )

https://www.linkedin.com/in/gihope

Ian is a general practicing member of the Association of Chartered Certified Accountants with fellowship status (FCCA). He is also a member of the Certified General Accountants Association of Canada (CGA), and a member of Chartered Professional Accountants of Canada (CPA).

Please Note – We aim to publish educational and value adding articles each month, for the benefit of our existing clients, prospective clients, and the wider public. So please FOLLOW US to take advantage of this valuable resource!

Learn more about our services

If you are the owner or manager or a limited company let QAccounting answer all your questions about how much to pay yourself in the new 2026-2027 tax year!

More Posts

April 2026: Mandatory Switch to Making Tax Digital (MTD) for Sole Traders and Landlords

The article helps the owners and managers of limited companies to understand what salary they should pay themselves in the new 2025-2026 tax year.

How Much Should I Pay Myself This Tax Year (2025 to 2026)?

The article helps the owners and managers of limited companies to understand what salary they should pay themselves in the new 2025-2026 tax year.

How will the UK Governments Recent Changes to Employers NI Impact my Business?

The article helps self-employed sole traders, limited companies, and partnerships to understand how the UK Government’s recent changes to Employer’s National Insurance will impact their business from April 2025.